Bitcoin has become a staple of the modern internet—and with it, the

blockchain. People say that blockchain technology will cause a

fundamental shift in how the internet works, how businesses function,

and just about everything else.

But what is blockchain?

Let’s cut through the marketing speak, technical jargon, and confusing explanations to figure out what blockchain really is.

Blockchains, Merged Mining, & ASICs: Lingo You Need To Know About Cryptocurrency Mining

Have you kept yourself

away from cyrptocurrencies or a discussion on their future? It's easy to

get lost in the lingo. Don't get left out with this handy reference

guide.

Read More

What Is Blockchain? The Simple Answer

A blockchain, in the most simple terms, is a distributed ledger.To understand what that means, we’ll first look at its opposite: a centralized ledger. Because blockchain technology got its start in finance, we’ll use the example of a bank.

Here’s what happens when you use your debit card:

- You swipe your card for a purchase at a store.

- The merchant sends a bill to your bank for the amount agreed upon.

- Your bank verifies that it’s likely you who authorized the purchase.

- The bank sends the money to the merchant.

- Finally, the bank makes a record of this information in its ledger.

That ledger is kept, maintained, and regulated by the bank. You might be able to read it in your online bank account, but you can’t change it. The bank is in complete control. If it decides to make a change, there’s nothing you can do about it.

Crucially, if a hacker gets access to the bank’s ledger, they can cause a lot of problems. They could change account balances, make it look like certain transactions never happened, and so on.

Which is why a distributed ledger is so cool.

If a bank operated on a distributed ledger, every member of the bank would have a copy of the ledger going back until the beginning of the bank’s existence. And whenever any member of the bank made a purchase, they’d tell every other member of the bank.

Each

member would verify the transaction and add it to the ledger (the added

record is called a “block”). This has some serious benefits, as there’s

no centralized authority that could manipulate the record. And hackers

getting access to one ledger wouldn’t be a huge problem, because the other ledgers could easily verify it.

How Bitcoin's Blockchain Is Making the World More Secure

Bitcoin's greatest

legacy will always be its blockchain, and this magnificent piece of

technology is set to revolutionize the world in ways we always thought

improbable... until now.

Read More

What Is Blockchain? The More Detailed Answer

As we saw above, a blockchain is a decentralized list of transactions. If I send James .02 Bitcoin, I’d send a message to everyone in the network saying “I’m sending James .02 Bitcoin” and they record the transaction.

But the transaction must be validated. And that’s where blockchain technology becomes a bit more complicated. Every Bitcoin wallet (we’ll get to that in a second) has a public key and a private key.

You use the private key to send a transaction request to the other members of the network, and they verify that you have the cryptocurrency in your account. If you do, they allow the transaction to register on the ledger.

The mechanics of the public/private key system are complex, but what it all comes down to is that each transaction is both verifiable and secure.

The

entire system, however, is computationally expensive. Everyone updating

the ledger needs to have a lot of power to verify transactions and

modify the ledger. That’s where mining comes in. The people who verify

and modify use their own computational resources and are rewarded with small transaction fees every time they do so.

Bitcoin is skyrocketing in value, but should you invest or is a crash coming? Let's look at what the future could hold for Bitcoin and its investors. Read More

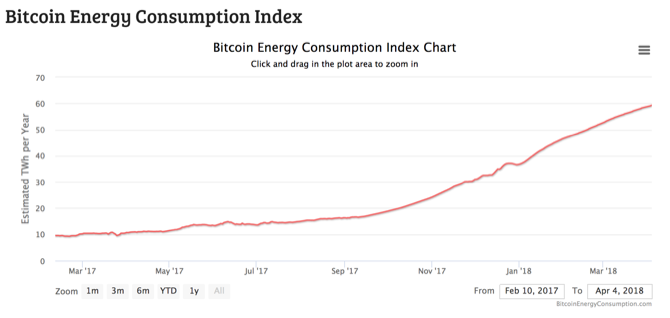

And they’re using a huge amount of electricity to do it. According to Digiconomist, Bitcoin mining consumes about as much electricity as all of Colombia.

It’s also very secure. To change a single block, you’d have to change every block that follows it. And after all that work, verification would fail, because the other copies of the chain would show that someone had tampered with one.

Someone could do it, but it would be astronomically difficult.

The Difficulty in Defining a Blockchain

While the mechanics behind blockchain technology aren’t always intuitive, it seems like it’s not too difficult to explain what a blockchain is. But what we’ve described here is only the traditional definition.

We can use this particular type of blockchain for a wide number of applications; cryptocurrency, sharing medical information, sending secure messages, and so on. But more blockchain-like technologies are in development for other uses.

For example, a company might use an internal blockchain to manage issue tracking in software. Each block on the chain could represent an issue, and users could post updates to the network. But is that a blockchain? The ledger isn’t public in this case—it’s only visible within the company.

Some people would say that makes it not a blockchain.

Other blockchain-like technologies aren’t encrypted. Are they still blockchains? What if it’s centrally managed, but uses other blockchain characteristics? What defines blockchain technology at the lowest level?

There’s no agreement on these matters.

What Is a Blockchain Wallet?

You’ll usually hear people talk about Bitcoin wallets, Ethereum wallets, and other cryptocurrency-specific wallets. But wallet technology could be used for any system using a blockchain.

The most important aspect of cryptocurrencies is keeping them safe after buying them! Learn about the most secure wallets for holding bitcoin and other cryptocurrencies. Read More

A wallet is a piece of software or hardware that “holds” your cryptocurrency. But it doesn’t actually hold anything—it’s simply a place that your public and private keys are stored. That information allows you to access the currency that the public ledger says you own.

The wallet is the only record of your keys. So if you lose it, you’ll no longer have access to your cryptocurrency.

Will Blockchains Change the World?

The decentralized nature of blockchain technology has many people talking about the democratization of the internet. And these claims might have some merit. But will blockchain fundamentally change how we communicate, do business, and run our lives?We’ll find out someday. In the end, the technology simply lets us verify transactions without running the risk of a centralized ledger.

We’ll find out someday. In the end, the technology simply lets us verify transactions without running the risk of a centralized ledger.